DeFi liquidity wars: What does the new Curve quadpool (4pool) mean for the OG tripool?

The term "Curve wars" shouldn't be strange to anyone who has dabbled in the DeFi space in one shape or form. Curve wars portray the ultimate fight for protocols looking to channel liquidity to their token by describing the peak of liquidity sorcery. Mainly described as a low-slippage decentralised exchange (DEX), Curve.fi represents yet the finest masterpiece in the form of a protocol that allows anyone to run permissionless savings accounts with better returns than traditional banking rates. Savers get the higher returns on Curve by accumulating the most veCRV tokens, a vote-escrow token that is used to influence the reward system on the platform.

One would have thought nothing could ever concern Do Kwon, CEO of Terraform Labs with Curve. Ah, the company behind the Luna-UST project revealed a new liquidity pool—the (UST-FRAX-USDC-USDT) 4pool on Curve. Needless to say, this 4D chess move has sparked a frenzy with discussions popping off on what remains of the future of Curve's OG tricrypto pool, the (DAI-USDC-USDT) 3pool, which was the standard, and the resurrection of the Curve's wars.

Curve's tripool (DAI-USDC-USDT)

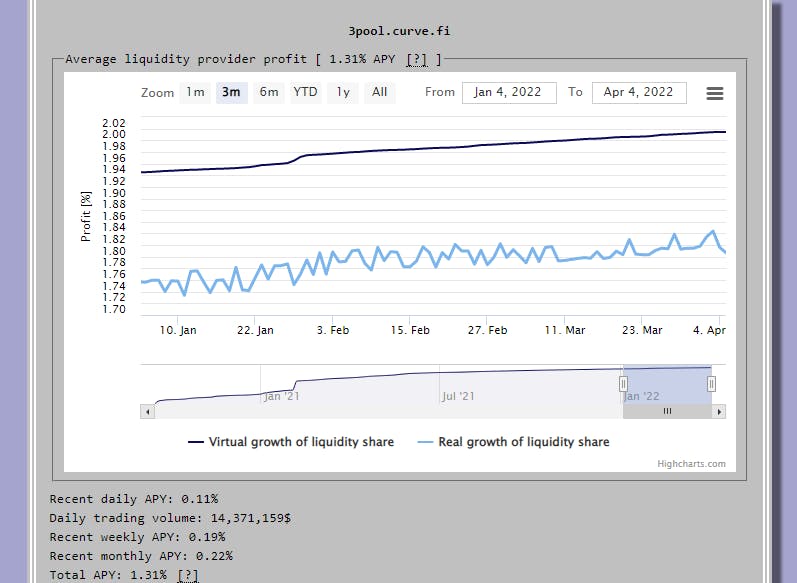

Curve introduced the triple stablecoin pool feature to deepen liquidity and reduce slippage significantly. The tripool is the most liquid pool with over $3 billion in deposits and the cheapest to conduct swaps because of its very low slippage (0.004%). A user who deposits one or two tokens in the pool balances out without affecting the user's returns. The implication is that once you deposit one stablecoin, it gets split over the three different coins in the pool giving the user exposure to all of them. The tripool contains the two biggest custodial/centralised stablecoins USDT and USDC, alongside DAI which many still criticise as being semi-decentralised. The implication of this is that centralised entities behind these stables present a single critical point of failure in the case of any regulatory clampdown that goes against the decentralised ethos of DeFi.

For instance, Center, an organisation run by Coinbase and Circle, two regulatory compliant US-based companies, is the custodian of USDC. USDC has an enormous scale within the DeFi ecosystem as it is the most paired stablecoin in most DeFi liquidity pools. The stablecoin makes up about 9% ($1.38 billion) of Curve's liquidity. In the case of an unprecedented regulatory clampdown such as geo-freezing of funds or accounts, DeFi could be significantly impacted. But beyond the Curve.fi platform, USDC is the second-largest asset on Uniswap, taking up $581 million of the total $3.9 billion locked in the protocol. It also makes up $3.5 billion of the $18.4 billion value locked in Compound and 4% and 13% in Aave and MakerDAO respectively, according to the DeFiant Terminal's data. USDC also represents a significant amount of DAI's underlying collateral.

Therefore, due to the heavy dependence on centralised stables for liquidity, a loss in confidence or failure of the USDC or USDT could result in a cascading effect that could bring DeFi to its knees, one thing many fear in this space. Hence, for the long term existence and sustainability of a truly decentralised DeFi ecosystem, there’s a need for a shift from centralised stables like USDC, USDT and DAI which are heavily (52.8%) backed by USDC (making it only quasi-decentralised).

The new sheriff in town - Terra's UST

Unlike USDC or USDT, TerraUSD (UST) is an algorithmic stablecoin that closely tracks the price of the US Dollar. UST is the native stablecoin of the Terra blockchain ecosystem developed by Terraform Labs using the Cosmos SDK. As an algorithmic stablecoin, UST relies on real-world asset reserves like cash or treasury bonds, a smart contract-based algorithm is used to keep the price of UST pegged to one dollar. A process that involves burning Terra's native LUNA token every time UST is minted and vice versa. Therefore through the resulting arbitrage opportunities, UST will always maintain its price peg to $1. LUNA's role in maintaining the price stability of UST has seen the price of the LUNA token rise astronomically, from $0.66 in 2021 and is currently sitting above $100 due to the significant demand for UST. Furthermore, UST recently flipped DAI to become the fourth largest stablecoin with over $16 billion in market cap. behind USDT, USDC, and BUSD. Do Kwon has since been beating the drums of war since the DAI flipping, a harbinger of more flipping underway.

The trailing criticisms

The Cambrian explosion the DeFi space has seen in $LUNA price following the increasing demand for the UST stablecoin has ruffled feathers across the DeFi community. As the $LUNA price continues to surge, critics are unsettled happing about an imminent Ponzi collapse for algorithmic stables like UST. One major reason for this doubt stems from the fact that the demand for UST largely comes from just one protocol in the Terra ecosystem, the Anchor protocol. The savings, lending and borrowing platform commands nearly 51% of Terra's total value locked (TVL). This is driven by the 20% fixed APY offered by Anchor. The lack of a balanced distribution across Terra's ecosystem has many people worried that a bank run on Anchor could dovetail into catastrophic effects that will cause the House of Terra to crash like a pack of cards. These concerns were further reinforced by the LUNA Foundation Guard's (LFG) action to inject $450 million into Anchor to sustain its high yield, further revealing the unsustainability of the promised APY in the long term.

twitter.com/RuneKek/status/1478166276979793..

Terra pushing strong - new strategies

But Do Kwon and his gang like to play 4D Chess! In response to the criticisms and perhaps recognising the truth in their critics' assertions, the LFG has started making moves to mitigate the risk of a possible bank run on the yield protocol, Anchor. The first of these was the $1 billion raised by the LFG which was set out for Bitcoin purchase. Then in March, Do Kwon, CEO of Terraform Labs, announced that the network was planning to purchase a whopping $10 billion in Bitcoin to serve as a reserve for the UST stablecoin to alleviate any selling pressure on $LUNA if it ever loses its peg to US dollar.

Changing the Curve terrain with the 4pool

For a while, two protocols led to the Curve wars. By removing the complexities of efficiently using the $CRV tokens, Yearn and Convex became yield optimizers that rotate assets between Curve's liquidity pools. Both protocols allow users to deposit $CRV tokens into their vaults, which then harvest rewards – both compounding the LP position and reinvesting in CRV to optimize yields. However, rather than locking CRV tokens on Curve.fi for the untradable $veCRV, Convex allows users to earn the same yield by depositing their $CRV into their vault and offers a tradable $vlCVX instead. And also gain additional rewards in Convex's $CVX token. This provided better opportunities for $CRV holders to lock up their tokens with Convex to earn more yields. This clearly set Convex apart as it rose to control a huge portion of the Curve's $veCRV tokens, making it the winner of the Curve wars. Therefore, LPs and protocols now compete for governance through bribing on Votium to accumulate $CVX. Whoever controls Convex, controls Curve's voting gauge.

The $DAI-$USDC-$USDT—3pool has been the central liquidity pool on Curve with over $3 billion in reserves. However, there's little incentive to provide liquidity to this pool beyond the low slippage it offers due to its deep liquidity. Currently, Terra and FRAX are the two largest holders of CVX on Curve and are also the two biggest providers of Votium incentives, with $4 million in UST and $7 million in FXS. This is significant because they are the biggest liquidity contributors to the 3pool. With the recent move to form a new liquidity pool, they can effectively dry up the 3pool, and drastically reduce the demand for the $1.5 billion DAI currently held in the 3pool.

The new 4pool — UST-FRAX-USDC-USDT

The declaration by Terra's Do Kwon in his tweet, "By my hand, $DAI will die" appears not to be a threat or joke. With the alliance formed between $UST, $FRAX, $USDC and $USDT and conspicuously leaving out DAI, the 4pool is about to stage a vampire attack on the 3pool as LPs and yield farmers seek higher returns with greater liquidity. This alliance will deepen liquidity for $UST and $FRAX stables due to the combined incentives of being used together rather than against each other. This increases the defensibility of both stablecoins during periods of demand contraction. The resulting high liquidity will also increase their peg stability and decrease de-pegging risk, further incentivising investors to deposit into the 4pool, creating a positive flywheel effect.

Checkmate - Are the Curve wars over?

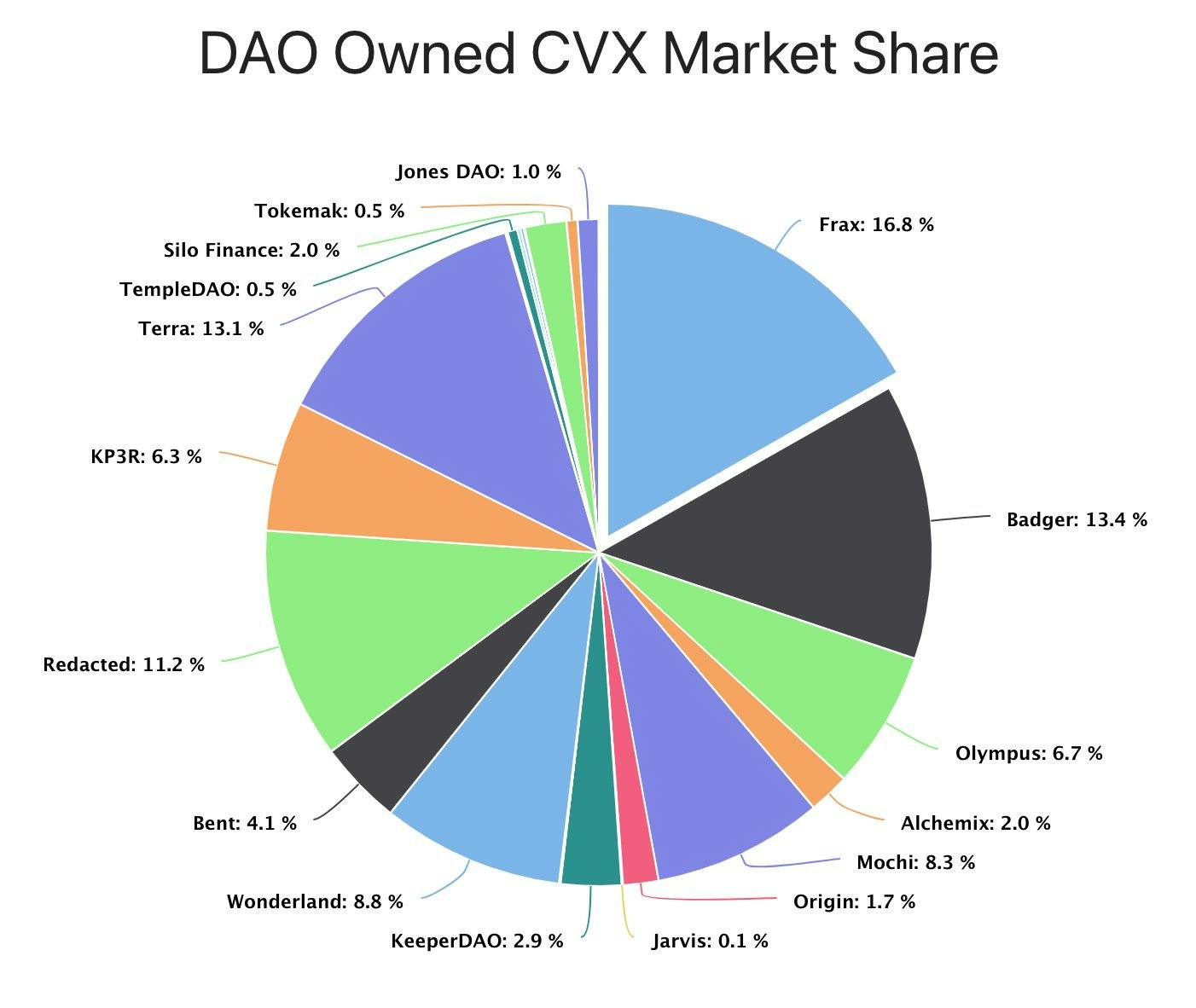

But the success of the 4pool is not guaranteed and still largely depends on liquidity incentives in the form of $CRV emissions. The higher the emissions, the more liquidity will be provided to the pool. As a chess player, Do Kwon knows this. To cement the success of this move, he is teaming up with Redacted Cartel, which holds the third-largest $CVX position. The result of this alliance will be the Cartel redirecting their voting powers to the 4pool, thereby significantly increasing incentives to provide liquidity to the 4pool. Cartel is also extending the Hidden Hand marketplace to the Terra ecosystem which provides more utility to the $UST. Also, with the likes of OlympusDao throwing their hat into the ring in support, the 4pool now boasts of a collective $CVX share of 47.8%. It seems like the Curve wars are over with the birth of a new deep pool.

Anchor, the ultimate beneficiary?

Recall the criticisms that trailed the yield protocol, Anchor and the unsustainability of Terra's LUNA token. With Anchor's payout rate depending on its yield reserves, the risk of a bank run on the UST will be greatly reduced as long as the 4pool becomes the new OG pool for DeFi. The logic here is simple, users now have a second yield option for their UST. There's no need of redeeming the UST for LUNA when you can deposit it in the 4pool and earn more yields, right? It seems like Do Kwon has managed to create the greatest "savings account" the crypto community has ever seen. A savings account that is accessible to protocols, LPs and institutions across every chain. Thereby, bringing the $UST stablecoin closer to becoming the de-facto standard for decentralised stablecoins across the entire DeFi ecosystem.

So what does this imminent dethronement of $DAI mean for DeFi?

With moves like these, $UST is rapidly positioning itself as the global monetary standard within DeFi's ecosystem. Of course, one could argue that, seeing as Ethereum is almost synonymous with DeFi as most DeFi activities take place on the network, that stable token native to the blockchain should be the de-facto standard. However, in an increasingly multi-chain ecosystem such as DeFi, there's a need for a more flexible, interoperable monetary standard. This is not to say that $UST is certainly that standard, but it currently fits the bill. As a native token to Terra built using the Cosmos SDK, it was fundamentally built for interoperability and can be rapidly integrated across networks. Moreso, its decentralised nature aligns it with the core ethos of DeFi and Crypto in general. Therefore, as the DeFi space evolves, having a completely decentralised monetary standard like $UST, backed by a completely decentralised reserve in Bitcoin, could be what is needed to take DeFi to the next level. And by decreasing the dependencies on centralised stables like USDC and USDT, DeFi can fully thrive, hence making it the ultimate beneficiary of all these innovations.